2026 Spring North American Mint

Overview: The exceptionally mild, warmer winter in the Pacific Northwest has allowed mint a head start for the growing season. It looks to be off to a good, healthy start. However, snowpack in Oregon, Washington, and Idaho was poor, creating early concerns about irrigation water availability. There will most likely be a reduction of water for some areas where surface water is a main source. After seeing increased supply and demand in peppermint and Scotch spearmint last year, growers are optimistic and increased new acres especially in the Idaho region. The limited supply of healthy rootstock to plant new fields remains a limiting factor. Midwest and Canadian growing areas had a more normal winter with cooler temperatures but overwintered generally well.

Competing Crops and Market Conditions:

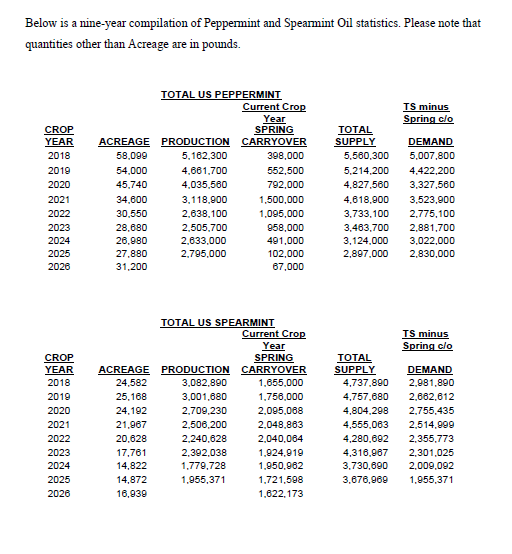

The softening of competitive crops heavily influences contract pricing and market dynamics. Growers are watching input costs, fuels, and equipment closely as margins are slim and high operating expenses continue to rise. Cattle prices remain highly competitive. Growers are cautiously optimistic about mint oil demands. However, growers continue to demand contracts over the volatility of the open market spot sales to secure longer-term financial stability. Spot sales throughout the winter were slow, but most buyers anticipated tight supply and purchased additional peppermint in the fall. Pricing for all varieties of mint remains unchanged from last year, and these prices will remain stable throughout the year. Despite current supply chain constraints and tight reserves for peppermint and Scotch spearmint, inventories are projected to stabilize. As harvest progresses, production is expected to fully meet current demand.

Mint Growing Areas – Spring Summary:

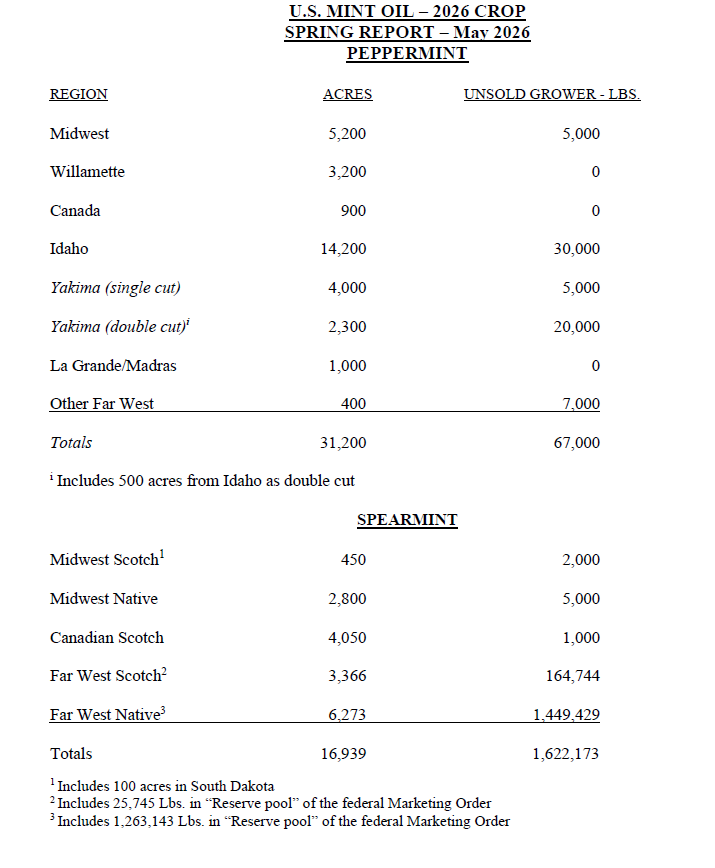

Idaho (Peppermint) – A growing number of new farmers are turning to peppermint as a viable crop. Competitive options are lacking and demand/pricing remains strong, making peppermint an attractive option. However, Idaho had a warm, dry winter with a poor snowpack, which has triggered concerns over water availability this summer.

Midwest – Midwestern growing regions experienced a typical winter with cool, damp weather, but as temperatures rise, crops show strong overwintering. This projects an average production year, with planted acres seeing a slight but stable increase.

Oregon (Peppermint) – Despite a mild winter with minimal snowpack causing concern for surface water sourced irrigation, an early spring allowed crops to get an excellent start and remain healthy. Overall, planted acreage has stabilized and is even up slightly across the region.

Washington (Peppermint) – The Columbia basin boasts a healthy water supply, but the Yakima region faces ongoing, lower water conditions closer to 40-50% of normal. Consequently, water rationing and state-declared drought conditions are already underway for the fourth consecutive year. While snowpack was poor, the mountains did receive ample rain to successfully fill reservoirs. Meanwhile, statewide peppermint acreage saw a slight increase with several growers resuming production.

Farwest Spearmint Growing Areas – Idaho, Utah, Oregon, and Washington:

Native Spearmint – Over the past year, rising demand nudged the price up slightly higher while acreage and supply remained stable. Far west Native inventory is at 186,286 pounds, and the new saleable is set at 43% for the year 2026-2027.

Scotch Spearmint – Scotch acres are up slightly but remain mostly flat for the Farwest, limited by shortage of clean root stock for new production fields and the need to rotate out older fields. The region’s current inventory sits at roughly 138,999 pounds, with the new saleable allotment established at 42% for the year 2025-2026.

Canada (Primarily Scotch) – The Alberta growing region had an average winter. While peppermint acreage remains flat in acres, Scotch is expanding to another 600-800 acres this spring. The additional production signals grower confidence and optimism towards the market future.

Conclusion:

Despite overall industry strength in North America, market demand growth has slowed, prompting some domestic manufacturers to reduce contracting volumes. While peppermint and Scotch spearmint acreage increased, and Native spearmint held steady, tight supplies of both peppermint and Scotch spearmint are expected to persist into next fall. Growers seek stable or improved pricing to offset rising fuel and fertilizer costs and are requesting multi-year contracts for added stability for this perennial crop. Consequently, accurate forecasting and forward contracting are essential to securing stable pricing for end-users.

India remains the primary competitor to North American mint oils. While recent tariffs temporarily slowed imports into the U.S., relaxed tariff rates have allowed material to resume flowing into the U.S. Ongoing systemic issues of adulteration with isolates and synthetics, pesticide residues, phthalate contamination, and other quality issues, along with lack of traceability continue to provide challenges to users.

Rising regulatory compliance costs across the supply chain are inflating prices and increasingly influencing the final pricing for end users and manufacturers. We believe that streamlining and consolidating required certifications could offer some relief in costs.

We are always available to answer any questions and help you and your company navigate the market conditions for favorable results.