2026 Spring North American Mint

Overview: The exceptionally mild, warmer winter in the Pacific Northwest has allowed mint a head start for the growing season. It looks to be off to a good, healthy start. However, snowpack in Oregon, Washington, and Idaho was poor, creating early concerns about irrigation water availability. There will most likely be a reduction of water for some areas where surface water is a main source. After seeing increased supply and demand in peppermint and Scotch spearmint last year, growers are optimistic and increased new acres especially in the Idaho region. The limited supply of healthy rootstock to plant new fields remains a limiting factor. Midwest and Canadian growing areas had a more normal winter with cooler temperatures but overwintered generally well.

Competing Crops and Market Conditions:

The softening of competitive crops heavily influences contract pricing and market dynamics. Growers are watching input costs, fuels, and equipment closely as margins are slim and high operating expenses continue to rise. Cattle prices remain highly competitive. Growers are cautiously optimistic about mint oil demands. However, growers continue to demand contracts over the volatility of the open market spot sales to secure longer-term financial stability. Spot sales throughout the winter were slow, but most buyers anticipated tight supply and purchased additional peppermint in the fall. Pricing for all varieties of mint remains unchanged from last year, and these prices will remain stable throughout the year. Despite current supply chain constraints and tight reserves for peppermint and Scotch spearmint, inventories are projected to stabilize. As harvest progresses, production is expected to fully meet current demand.

Mint Growing Areas – Spring Summary:

Idaho (Peppermint) – A growing number of new farmers are turning to peppermint as a viable crop. Competitive options are lacking and demand/pricing remains strong, making peppermint an attractive option. However, Idaho had a warm, dry winter with a poor snowpack, which has triggered concerns over water availability this summer.

Midwest – Midwestern growing regions experienced a typical winter with cool, damp weather, but as temperatures rise, crops show strong overwintering. This projects an average production year, with planted acres seeing a slight but stable increase.

Oregon (Peppermint) – Despite a mild winter with minimal snowpack causing concern for surface water sourced irrigation, an early spring allowed crops to get an excellent start and remain healthy. Overall, planted acreage has stabilized and is even up slightly across the region.

Washington (Peppermint) – The Columbia basin boasts a healthy water supply, but the Yakima region faces ongoing, lower water conditions closer to 40-50% of normal. Consequently, water rationing and state-declared drought conditions are already underway for the fourth consecutive year. While snowpack was poor, the mountains did receive ample rain to successfully fill reservoirs. Meanwhile, statewide peppermint acreage saw a slight increase with several growers resuming production.

Farwest Spearmint Growing Areas – Idaho, Utah, Oregon, and Washington:

Native Spearmint – Over the past year, rising demand nudged the price up slightly higher while acreage and supply remained stable. Far west Native inventory is at 186,286 pounds, and the new saleable is set at 43% for the year 2026-2027.

Scotch Spearmint – Scotch acres are up slightly but remain mostly flat for the Farwest, limited by shortage of clean root stock for new production fields and the need to rotate out older fields. The region’s current inventory sits at roughly 138,999 pounds, with the new saleable allotment established at 42% for the year 2025-2026.

Canada (Primarily Scotch) – The Alberta growing region had an average winter. While peppermint acreage remains flat in acres, Scotch is expanding to another 600-800 acres this spring. The additional production signals grower confidence and optimism towards the market future.

Conclusion:

Despite overall industry strength in North America, market demand growth has slowed, prompting some domestic manufacturers to reduce contracting volumes. While peppermint and Scotch spearmint acreage increased, and Native spearmint held steady, tight supplies of both peppermint and Scotch spearmint are expected to persist into next fall. Growers seek stable or improved pricing to offset rising fuel and fertilizer costs and are requesting multi-year contracts for added stability for this perennial crop. Consequently, accurate forecasting and forward contracting are essential to securing stable pricing for end-users.

India remains the primary competitor to North American mint oils. While recent tariffs temporarily slowed imports into the U.S., relaxed tariff rates have allowed material to resume flowing into the U.S. Ongoing systemic issues of adulteration with isolates and synthetics, pesticide residues, phthalate contamination, and other quality issues, along with lack of traceability continue to provide challenges to users.

Rising regulatory compliance costs across the supply chain are inflating prices and increasingly influencing the final pricing for end users and manufacturers. We believe that streamlining and consolidating required certifications could offer some relief in costs.

We are always available to answer any questions and help you and your company navigate the market conditions for favorable results.

2025 Spring North American Mint Outlook

Overview: Mint oil sales are picking up and storage oil is getting tight across all types, especially peppermint and scotch spearmint. After many years of the market being sluggish, we are seeing an increase in movement which in turn is tightening up the storage oil supply and driving prices up. Mint acres seem fairly flat with an upwards trend in increased production. Growers are demanding long-term contracts to plant more acres. All spring planting is done by now and is off to a good start with adequate water supply.

Competing Crops and Market Conditions: Competitive crops continue to be potatoes, onions, sugar beets, soybeans, corn, and dairy cows. However, pricing has dropped and acres are being cut in those commodities making mint an attractive crop to grow. We continue to hear that farmers want to grow more mint but also want multi-year contracts to ensure profitability. All types of oil movement have been steady throughout the winter and spring but have really picked up this spring in peppermint cleaning out any quality storage oil to the point that there isn’t much left other than off quality oil. Scotch spearmint has flipped from the last two years of being over supplied and acres being taken out to now new acres are being planted and most farmers are fully contracted for the 2025 crop year and in addition little excess storage oil is available. Pricing is moving up in all types but mostly peppermint and scotch with supply being tight. The peppermint market is changing quickly this spring with high demands in contracting and spot purchasing. Most growers are moving peppermint oil if they have any in storage, significantly reducing availability to almost nothing this spring. Peppermint oil will be very tight this year with the majority contracted already and new acres planted are not following quickly behind this which could lead to a very tight year and perhaps high pricing.

Mint Growing Areas – Spring Summary Idaho (Peppermint) – Acres in Idaho remain flat or slightly up this year as wilt is a factor in planting new acres for established growers. Most acres are conservatively contracted and farmers expect to have some extra for the spot market. Idaho received a good snowpack and an early dry spring allowing new acres to planted on time but requiring starting water right away with the warm temperatures.

Midwest – The Midwest growing areas have had an average spring and winter providing time to get into the field this spring and get any planting done in good moisture. Some new acres have been planted on peppermint and replacement acres. Spearmint types are mostly flat but perhaps up slightly.

Oregon (Peppermint) – The water supply across the state looks to be exceptionally good with snowpack over 100% including the madras area. Planted acres of peppermint remain flat. Some farmers have commented for the first time about power costs going up 40% over the last two years making irrigation a significantly higher cost for mint production.

Washington (Peppermint) – The Columbia basin is in good shape for water as usual, but the Yakima area is closer to 60% of normal water and starting the irrigation season off with rations already and reduced water supply. Most of the state didn’t see the typical snowpack with a mild winter and early warm spring. This would make year three of a state declared drought. Peppermint acres remain flat for the state. Most growers that grow peppermint are running out of clean wilt free ground and long term will continue to see a reduction in peppermint.

Farwest Spearmint Growing Areas – Idaho, Utah, Oregon, and Washington:

Native Spearmint – Growers voted to increase saleable for the new year and a 2% increase for the 2024 growing year but with the new political administration it’s looking unlikely the increase will go through. There is plenty of pool oil but with the saleable low its driving prices higher than the previous year and available supply could be tight. Farwest Native inventory is at 206,750 pounds and the new saleable is set at 39% for the year 2025-2026.

Scotch Spearmint – Scotch acres have increased as demand has picked up and pricing improved. The current inventory is about 205,585 pounds, and the new saleable allotment is 36% for the 2024-2025 year.

Canada – (Primarily Scotch) – The Alberta growing region had an average winter with lighter than normal snowpack and irrigation is set to give 80% of normal but should be sufficient for growing mint. Scotch spearmint has taken a quick turn from being down acres to planting an additional 800 acres to help meet the demands in the quickly changing market. Peppermint acres will remain the same in this region. The tariffs are a big concern in Alberta and could change contracting if tariffs get hit hard.

Conclusion – The mint oil market has been very active this year with increased demands. Peppermint and Scotch spearmint will be in very tight supply this year. India continues to be the major competitor to North America Mint Oils but systematic issues of adulteration with isolates and synthetics, pesticide residues, phthalate contamination and other quality issues as well as the lack of traceability continue to provide challenges to users.

Regulatory demands and the associated costs continue to rise throughout the supply chain to the point where it is becoming a factor in final pricing to the end-user/manufacturers.

We are always available to answer any questions and help you and your company navigate the market conditions for favorable results.

U.S. MINT OIL – 2021 CROP SPRING REPORT – MAY 2021

CURRENT CROP CONDITION

In general, North American mint plantings have over-wintered well. Rain and snowfall have been below average but there was sufficient winter moisture to maintain healthy rootstocks.

Irrigation water supplies may be tight, but adequate for mint production in the far west regions. One significant trend which may portend the future, is that the primary irrigation water source for the southern Oregon/northern California region has been shut off completely because of environmental issues. Although this area is not large enough to significantly affect supply, it causes concern for availability of irrigation water in the future.

MARKET CONDITIONS

Peppermint – Overall demand for North American peppermint oil continues to be slow. We see steady demand in the oral care industry and weak demand in the confectionery industry. For a brief period this winter, prices paid to the producer dropped below market price and growers in

weak financial condition liquidated their stocks. This left unsold inventories in strong financial ownership and prices rebounded some. Less than average quantities of the 2021 crop are pre-sold on a contractual basis and we expect that industry demand will continue to be dull. This may well lead to further reduction of acreage for the 2022 crop and could lead to a tighter supply situation by 2023 crop year. As compared to this date one year ago, peppermint acreage has declined an additional 19%, unsold carryover stocks have increased 89% and market volume demand has declined 25%

Spearmint – As has been the situation for a number of years, the only significant production and supply of natural spearmint oil worldwide is North America. Global demand for spearmint oil continues to be steady. Due to good supply prices have weakened some and growers are responding by slowly reducing acreage. As compared to this date one year ago, acreage in production has declined 11.7%, unsold carryover stocks have declined 2.2% and market volume demand has increased by 3.5%

LAVANDE / LAVANDIN HE – CROPS 2020

As harvest is over, it is now reasonable to suggest a realistic trend. In short, it was good !

Overall, production figures are expected to be 20-30% higher than last year. An exception to notify for Lavandin Super which encountered difficulties because of reduction in planted areas and disease.

All lights are therefore on green so that can be expected a drop in prices, but in what proportion …, this is the only unknown at this date.

We will have to wait a few more weeks for everyone to play its cards in an unusual configuration: health crisis and new trade rules oblige!

RAPPORT RECOLTE 2020 LAVANDE / LAVANDIN HE

La récolte terminée, il est désormais raisonnable d’évoquer une tendance réaliste de cette dernière. En un mot, elle a été bonne !

Dans l’ensemble, devraient être annoncés des chiffres de production supérieurs à ceux de l’année dernière de l’ordre de 20 à 30 %. Un bémol pour le Lavandin Super qui rencontre des difficultés car touché par le dépérissement et la réduction des surfaces plantées.

Tous les feux sont donc au vert pour que l’on assiste à une baisse des prix mais dans quelle proportion… , c’est la seule inconnue à ce jour.

Il faudra patienter encore quelques semaines pour que chacun abatte ses cartes dans une configuration inhabituelle : crise sanitaire et nouvelles politiques commerciales obligent !

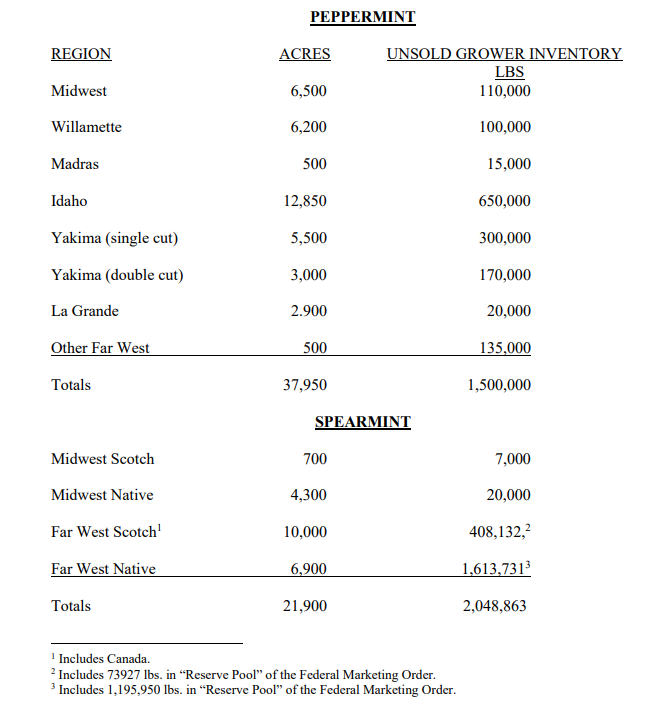

U.S. MINT OIL – 2020 CROP

U.S. MINT OIL – 2020 CROP

SPRING REPORT – MAY 2020

PEPPERMINT

REGION ACRES UNSOLD GROWER INVENTORY

LBS

Midwest 8,200 60,000

Willamette 7,200 50,000

Madras 500 7,000

Idaho 15,500 550,000

Yakima (single cut) 7,000 240,000

Yakima (double cut) 4,000 230,000

La Grande 3,400 35,000

Other Far West 1,640 120,000

Totals 47,400 1,292,000

SPEARMINT

Midwest Scotch 800 5,000

Midwest Native 5,300 2,000

Far West Scotch1 9,900 340,523,2

Far West Native 8,800 1,747,5453

Totals 24,800 2,095,068